The rising debt-to-income (DTI) ratio is causing concern among house purchasers.

Despite the benefits of reduced borrowing rates in the aftermath of the Coronavirus outbreak, house purchasers say their DTI ratio has gotten out of hand.

Home purchasers in India are now dealing with a considerably greater debt-to-income (DTI) ratio than ever before, thanks to record low-interest rates on family savings, significant unemployment, and growing inflation levels. Despite the benefits of lower interest rates in the aftermath of the Coronavirus outbreak, their DTI ratio has suddenly risen to levels that are unmanageable.

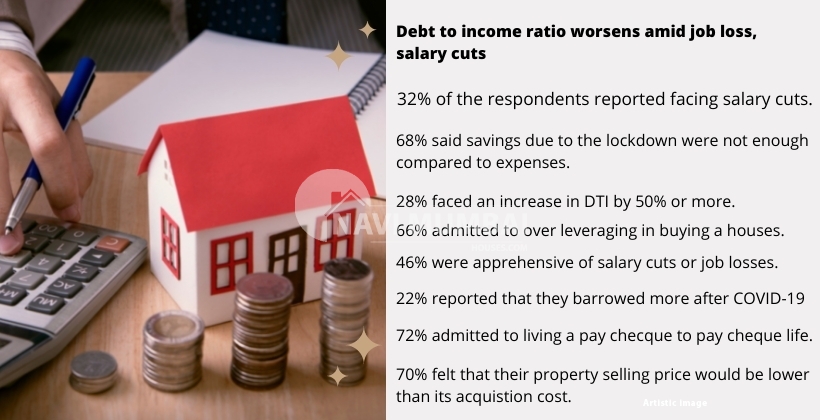

Following COVID-19, new purchasers are playing it safe and keeping their LTV (loan-to-value) as low as possible. Existing purchasers, on the other hand, are becoming increasingly anxious. According to an online poll conducted by Track2Realty, over one-third of respondents (32%) stated they had to take wage cutbacks as a result of the epidemic, and 68 percent stated their reserves were insufficient to compensate for the wage decrease.

Are you looking for a 3 BHK Apartment on Rent in Kharghar Navi Mumbai? Then you may contact Navimumbaihouses.com the biggest property portal to Rent / Sale / New Projects properties in Kharghar and Navi Mumbai.

As a result of job losses and wage cuts, the debt-to-income ratio is worsening.

Take, for example, communication expert Naman Gupta. When he bought a property in 2017, his salary was Rs 1 lakh, and his DTI ratio was at a healthy 40 percent. Despite a decreased interest rate, his DTI ratio has risen to moreover 50% now that his wage has been reduced by 30%. As a result, it is harming his day-to-day spending. “We all anticipate employment growth, not employment de-growth. I expected a 20 percent pay increase when I signed up for an EMI of Rs 40,000. It would have effectively kept my DTI at a comfortable level of approximately 30%. However, I am now in a bind, and with limited finances, it would be difficult for me to continue servicing the EMIs in order to keep the property for a long time,” Gupta said.

Gupta isn’t the only one whose DTI has risen unexpectedly. According to the poll, 28% of Indian consumers said that their DTI ratio had risen to 50% or above. Even more, concerning for existing property purchasers is the fact that, following the second wave of COVID-19, 46% of Indians are concerned about potential income cutbacks or job losses.

In addition, 64% of purchasers claimed to have over-leveraged their financial resources and living with a greater DTI ratio. “Yes, I do agree that I over-leveraged in my property purchase, but I did not have the liberty of choice,” says S Ramaswamy, a software expert. In places like Bengaluru, you have two options: pay a premium price for a property or pay greater rent.” In the post-pandemic period, however, 22% of respondents said they had borrowed extra in order to maintain their livelihood and pay their housing EMI.

Will the COVID-19 epidemic lead to a rise in mortgage defaults?

According to data issued by the Reserve Bank of India (RBI), India’s household financial savings rate fell to 10.4% of GDP in the July-September 2020 quarter, down from 21% the previous quarter. According to RBI statistics issued in 2020, family income increased at a compound annual growth rate (CAGR) of 4.3 percent, compared to a 17.7 percent CAGR rise in borrowing by families or people, as measured by the compensation and wages bill of the country’s top listed corporations. As a result, it should come as no surprise that 72 percent of respondents acknowledged living paycheck to paycheck after purchasing a property.

Would this result in a rise in foreclosures and short sales in the property market? Unfortunately, there is no obvious solution, since 70% of purchasers say that the selling price on the secondary market today is significantly lower than their whole purchasing cost. “A distressed sale now would be a big waste of money. Prachi Desai, a Mumbai resident, adds, “We’ll never be able to purchase a property again.”

If You’re Looking for a Rental home in Navi Mumbai We Have the Best Option For You 3 BHK Flat for Rent in Kharghar Navi Mumbai: https://navimumbaihouses.com/3-bhk-flats-for-rent-in-kharghar/

What does the perfect DTI ratio look like?

The debt-to-income ratio (DTI) is a quantitative economic metric that divides gross monthly income by debt. This is how lenders decide if a potential borrower is qualified and capable of repaying the amount. Empirical evidence from housing loans suggests that borrowers with a DTI ratio of greater than 50% are more likely to default on their home loan EMIs.

In most developed nations throughout the globe, financial experts recommend following the ‘28/36 rule,’ which states that household expenditure should not exceed 28 percent of gross monthly income and debt should not exceed 36 percent. In other areas of the globe, a DTI ratio of 36 percent to 43 percent shows that the borrower has less room to handle any unplanned expenditure, and 50 percent or greater is a definite red signal. However, in India, it is a reality for a large number of purchasers, and this is getting painful for property purchasers as a result of job losses and pay cuts.

Any suggestions

Experts advise that while purchasing a home, one should be more practical than emotional to avoid potential loan defaults and foreclosure. “When you’re dealing with an untenable DTI ratio, there are just two options. One option is to sell other funds and assets to pay as much as possible to the bank upfront and decrease the EMI. If you have no alternative funds, you should go to your bank about it right away and, noting your new financial condition, request a loan restructuring for a longer term to keep your EMI low,” says Amitabh Sinha, an economist.

We are the online real estate portal to buy sell and rent properties in Navi Mumbai, Mumbai, and Thane. We can help you buy properties at affordable prices at your desired location. For more information call us on +91 8433959100

If you want daily property update details please follow us on Facebook Page / YouTube Channel / Twitter

Describe Fungible FSI